Key Advantages of Buying a Home Today - Thursday December 8th, 2022

Ian Walterhouse

Thursday, December 8, 2022

Key Advantages of Buying a Home Today

There’s no doubt buying a home today is different than it was over the past couple of years, and the shift in the market has led to advantages for buyers today. Right now, there are specific reasons that make this housing market attractive for those who’ve thought about buying but have sidelined their search due to rising mortgage rates. Yes, that’s right, even in light of yesterday's interest rate increase now is a good time to buy.

Buying a home in any market is a personal decision, and the best way to make that decision is to educate yourself on the facts, not following sensationalized headlines in the news today. The reality is, headlines do more to terrify people thinking about buying a home than they do to clarify what’s actually going on with real estate.

Here are five reasons potential homebuyers should consider buying a home today.

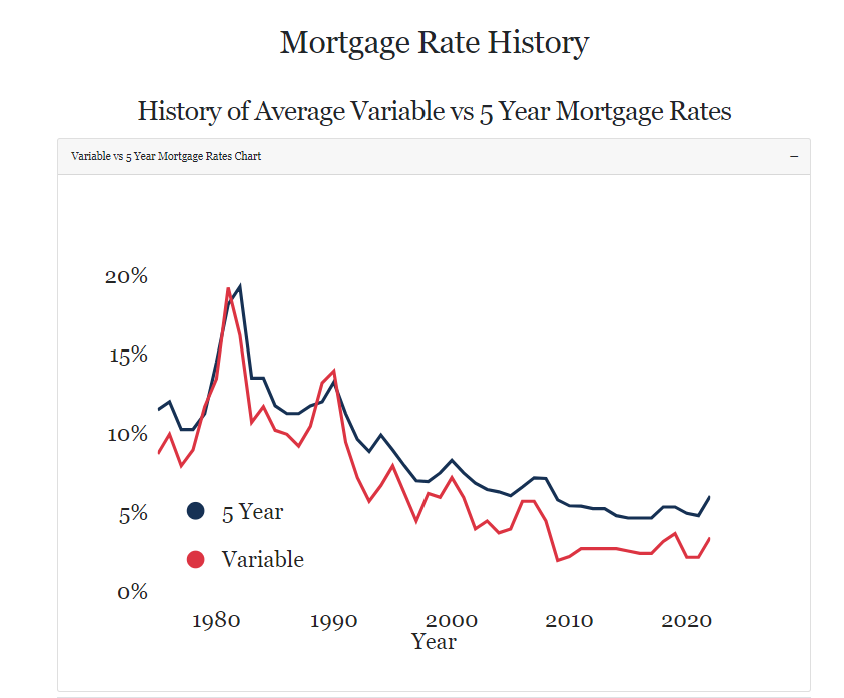

1. Today’s High Interest Rates are Actually Historically Very Low

Let’s dig into some historic context to put things in perspective.

In Canada, in 1981, the variable mortgage rate was 19.20%. In 1984, 11.7%. In 1990, it was 13.95%. The graph below shows Canadian interest rates over a 40+ year range.

Many people, even first time home buyers, bought homes when mortgage rates were more than four times as high as they are today. Historic data shows that today’s “high” interest rates are relatively very low over the last 30 years. Peaks and valleys of housing prices and mortgage rates are part of the housing market cycle.

Ultimately, the factors that determine your ability to buy in the short run considers home prices and your ability to service your mortgage payments. We love the term marry the house and date the rate. If you are a first time home buyer, you are likely to hold a mortgage for 20 plus years. You have options for shorter term mortgage products with lower rates, or longer term products with historically very low rates (they are just higher than the historic lows most recently recorded).

Talk to anyone who lived through the 1980s when 18% interest rates to know home ownership is very much a possibility regardless of rates. We suggest revisiting your qualifications with a real estate agent and mortgage broker to work out the scenarios of your particular situation within the current market conditions.

2. Fewer Homes on the Market Means Less Competition

There are always people who are making a move - even when market conditions are changing. If you are looking to buy right now, you will face less competition from other buyers. Multiple offers are few and far between as are sale prices over asking. And if you are looking to sell, you will have fewer homes in competition with yours.

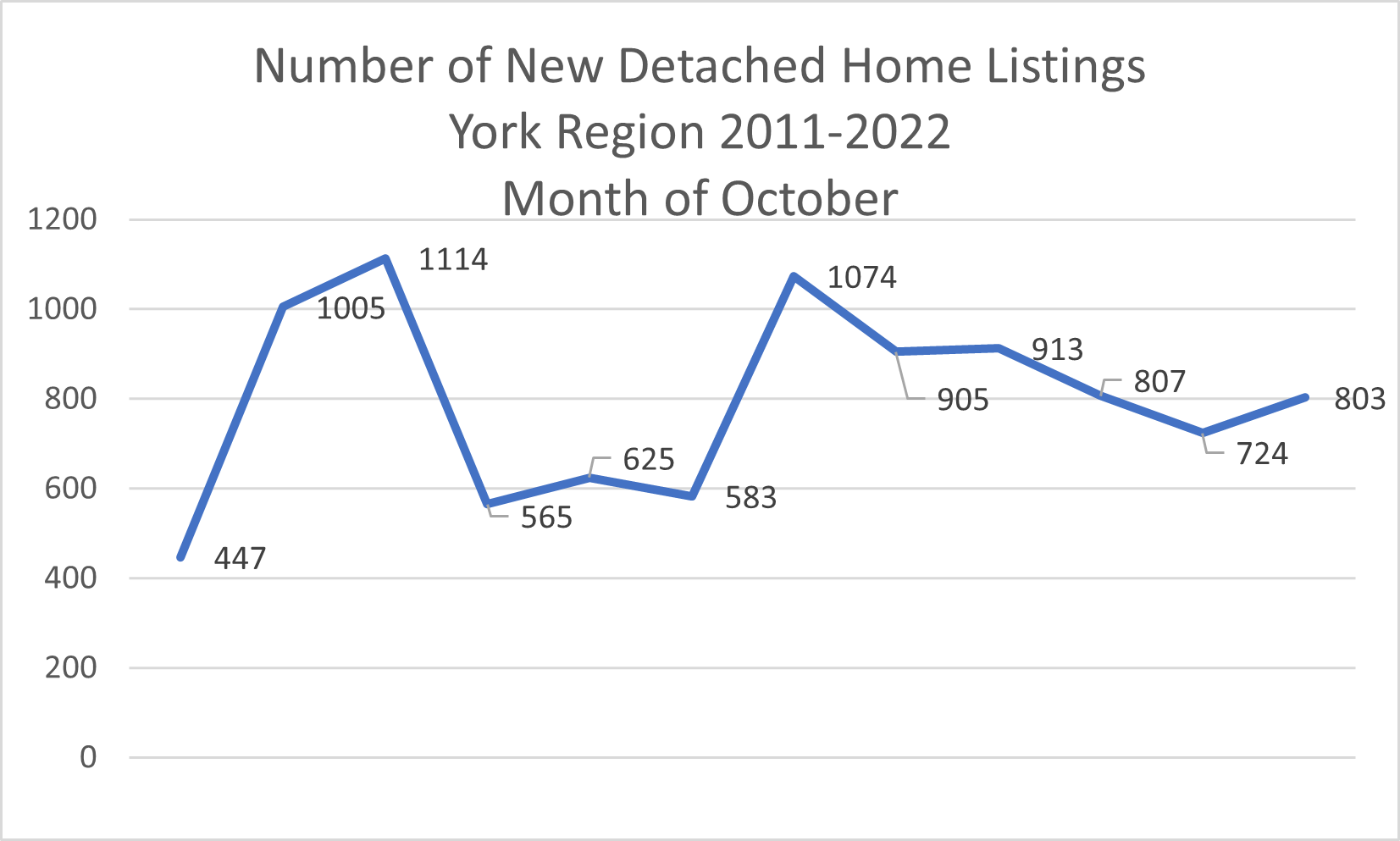

According to data from the Toronto Real Estate Board, the decline in the number of new homes for sale in York Region is not dissimilar to the 2017/2016 market correction. The graph below shows data for the month of October in each calendar year listed. The average number of homes for sale in the month of October between 2011 and 2022 is 797 homes. While the 2022 is below that number, it is not signaling anything but a predictable reaction to a series of swift mortgage rate increases and a response to the historic high levels of activity over the last two years of the pandemic.

3. Growth in the Rest of Canada and the US Shows Likely Market Trend of More Average Rates of Buying and Selling

According to the Canadian Real Estate Association, the number of newly listed homes was up 2.2% on a month-over-month basis in October, with gains in the Greater Toronto Area (GTA) and the B.C. Lower Mainland offsetting declines in Montreal and Halifax-Dartmouth.

“In October, sales across the country increased for the first time since before interest rates started to rise last winter,” said Jill Oudil, Chair of the Canadian Real Estate Association. “Of course, we’ve known the demand was there, so it’s just been a matter of some playing the waiting game as borrowing costs and prices have adjusted. Moving into 2023, sellers and buyers will likely continue coming off the sidelines, but it’s a very different market compared to just one year ago.” continued Oudil.

“October provided another month’s worth of data suggesting the slow down in Canadian housing markets is winding up,” said Shaun Cathcart, CREA’s Senior Economist. “Sales actually popped up from September to October, and the decline in prices on a month-to-month basis got smaller for the fourth month in a row."

There were 3.8 months of inventory on a national basis at the end of October 2022, up slightly from 3.7 months at the end of September. While the number of months of inventory is still well below the long-term average of about five months, it is also up quite a bit from the all-time low of 1.7 months set at the beginning of 2022.

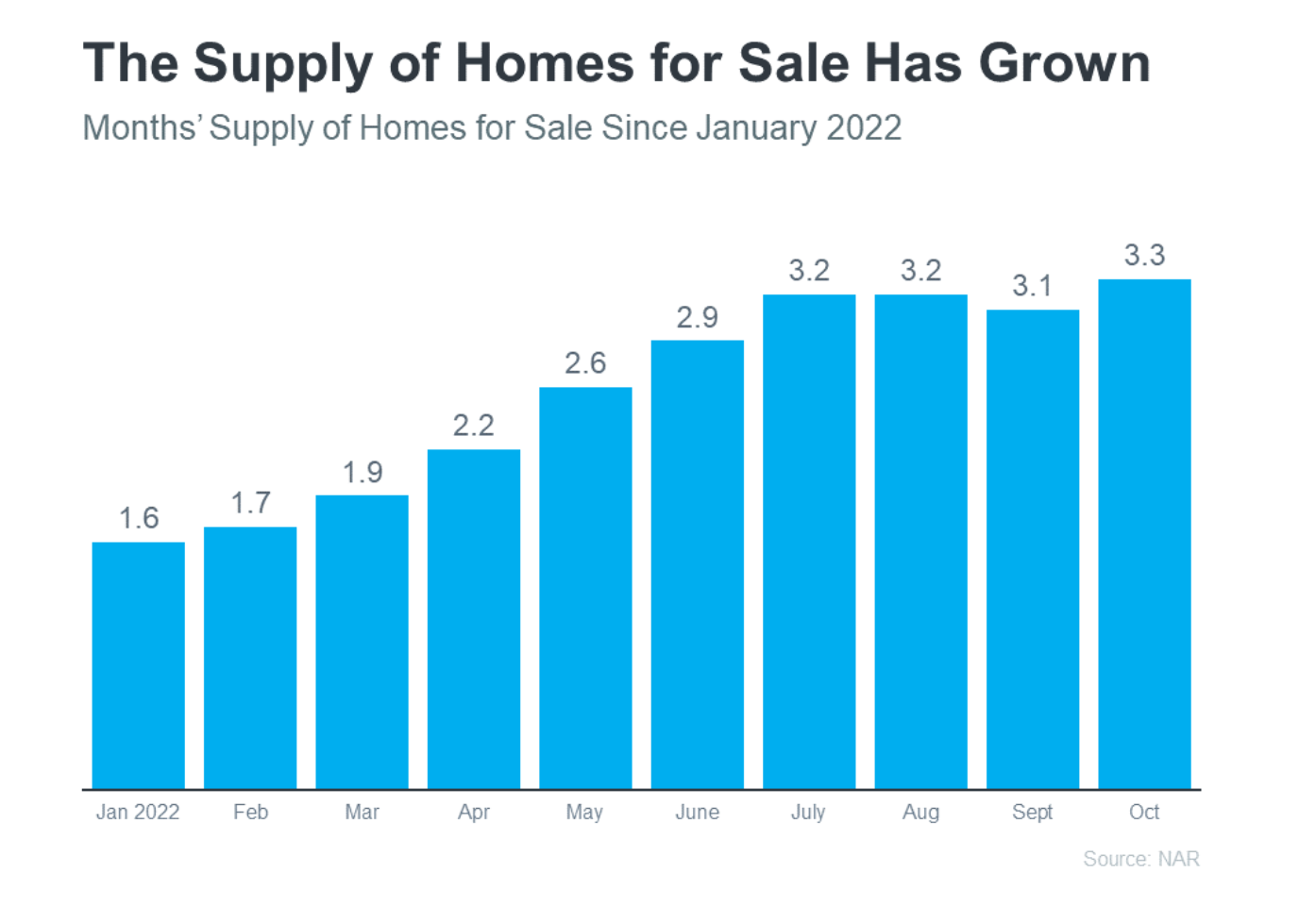

In the United States, according to data from the National Association of Realtors (NAR), this year, the supply of homes for sale has grown significantly compared to where it started the year.

This growth has happened for two reasons: homeowners listing their homes for sale and homes staying on the market a bit longer as buyer demand has moderated in response to higher mortgage rates.

The good news for you is that even slight growth in the number of homes for sale means that you have more homes to choose from. And, again, when there are more homes on the market, you could also see less competition from other buyers because the peak frenzy of competing over the same home has eased too.

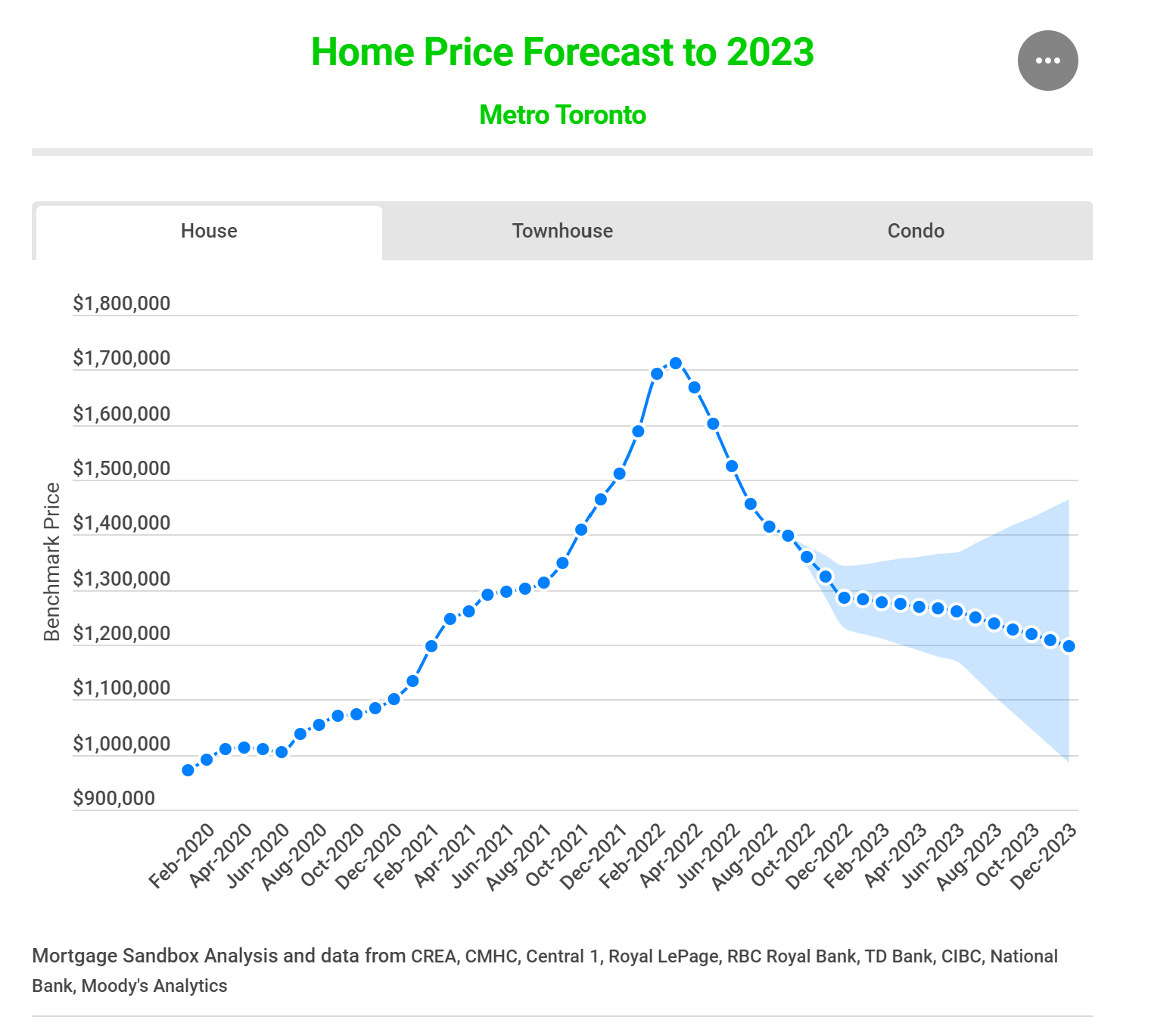

4. Home Prices Are Not Projected To Crash

Experts don’t believe home prices will crash like they did in 2008. Instead, home prices will moderate at various levels depending on the local market and the factors, like supply and demand, at play in that area. That’s why some experts are calling for slight appreciation and others are calling for slight depreciation (see graph below):

While prices continue to decline throughout the GTA, Toronto Regional Real Estate Board CEO John DiMichele emphasizes the effect will be temporary.

If you consider the big picture and average the expert forecasts for 2023 together, the expectation is for relatively flat or neutral price appreciation next year. So, if you’re worried about buying a home because you’re afraid home prices will crash like they did in 2008, rest assured that’s not what expert projections tell us.

5. Mortgage Rates Have Risen, but They Will Come Down

While mortgage rates have risen dramatically this year, the rapid increases we’ve seen have moderated in recent weeks as early signs hint that inflation may be easing slightly. Where they’ll go from here largely depends on what happens next with inflation. If inflation does truly begin to cool, mortgage rates may come down as a result.

Current predictions, as reported before yesterday’s increase, are still useful context. According to Canadian Real Estate Wealth (https://www.canadianrealestatemagazine.ca), show that even though rates may not dip as low as they have been over the last several years, the rates are likely to lower in the short term.

Benjamin Tal and Karyne Charbonneau each of whom are chief economists for CIBC, note that given the September 2022 rate increase, they expect the Bank of Canada will call it a day, leaving the overnight target rate at 3.25% “for the duration of 2023.” While CIBC doesn’t see any further rate hikes in 2023, in examining the economic factors, it also doesn’t expect the Bank of Canada to begin easing rates any sooner than 2024.

Altruafinancial.ca believes that the main tool we have when reading the current mortgage rate market is the Government of Canada bond market yield. Currently, the Canadian bond markets are priced in anticipation of a further 0.75% increase in Central Bank of Canada rates in 2022- early 2023 or perhaps even slightly higher.

In its short to medium-term Canadian interest rate predictions, TD Economics projected the Bank of Canada to increase rates in the fourth quarter and maintain the level until the end of 2023. TD Economics predicted the Canadian central bank to lower the policy rate to 2.90% in 2024, 2.05% in 2025, 2% in 2026 and 2% in 2027.

Scotiabank expects the Bank of Canada to raise its overnight rate to 3.5% in the fourth quarter of 2022 and maintain the rate throughout 2023.

ING's forecast expects the Bank of Canada to have a further 75 base points of hikes, bringing the overnight rate to 4% in the fourth quarter of 2022, dropping to 3.75% in the third quarter and 3.25% in the fourth quarter of 2023 respectively.

When a decrease happens, expect more buyers to jump back into the market. For you, that means you’ll once again face more competition. Buying your house now before more buyers reenter the market could help you get one step ahead.

When mortgage rates come down, those waiting on the sidelines will jump back in. Your advantage is getting in before they do.

Bottom Line

If you’re thinking about buying a home, you should seriously consider the advantages today’s market offers. Let’s connect so you can make the dream of homeownership a reality.

We would like to hear from you! If you have any questions, please do not hesitate to contact us. We are always looking forward to hearing from you! We will do our best to reply to you within 24 hours !